Documentation

This page presents an in depth documentation of our machine-learning models trained on historical data. Results are presented for research and analytical purposes only.

LSTM (Long Short-Term Memory)

Deep LearningA deep learning model that predicts next-step log returns using an LSTM architecture trained on historical OHLCV data. Predictions are reconstructed back to price levels for evaluation and charting.

How It Works

- Pulls market data from Alpaca Bars (equities or crypto pairs)

- Builds sliding windows over the chosen lookback period

- Target at time t+1: r_{t+1} = log(close_{t+1} / close_t)

- Prediction made from window ending at t: predict r_{t+1}, then reconstruct close_{t+1}

Visualizations

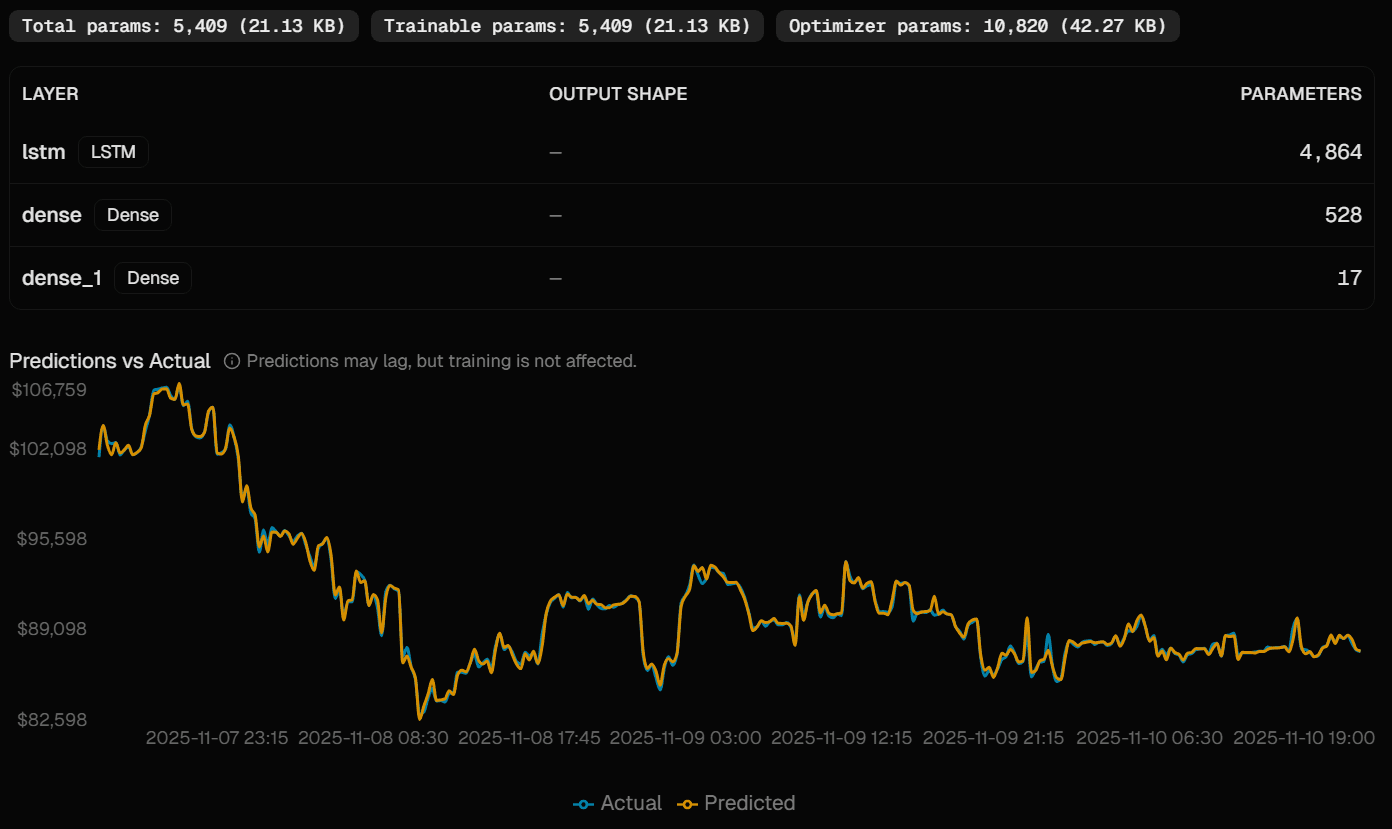

Model Architecture

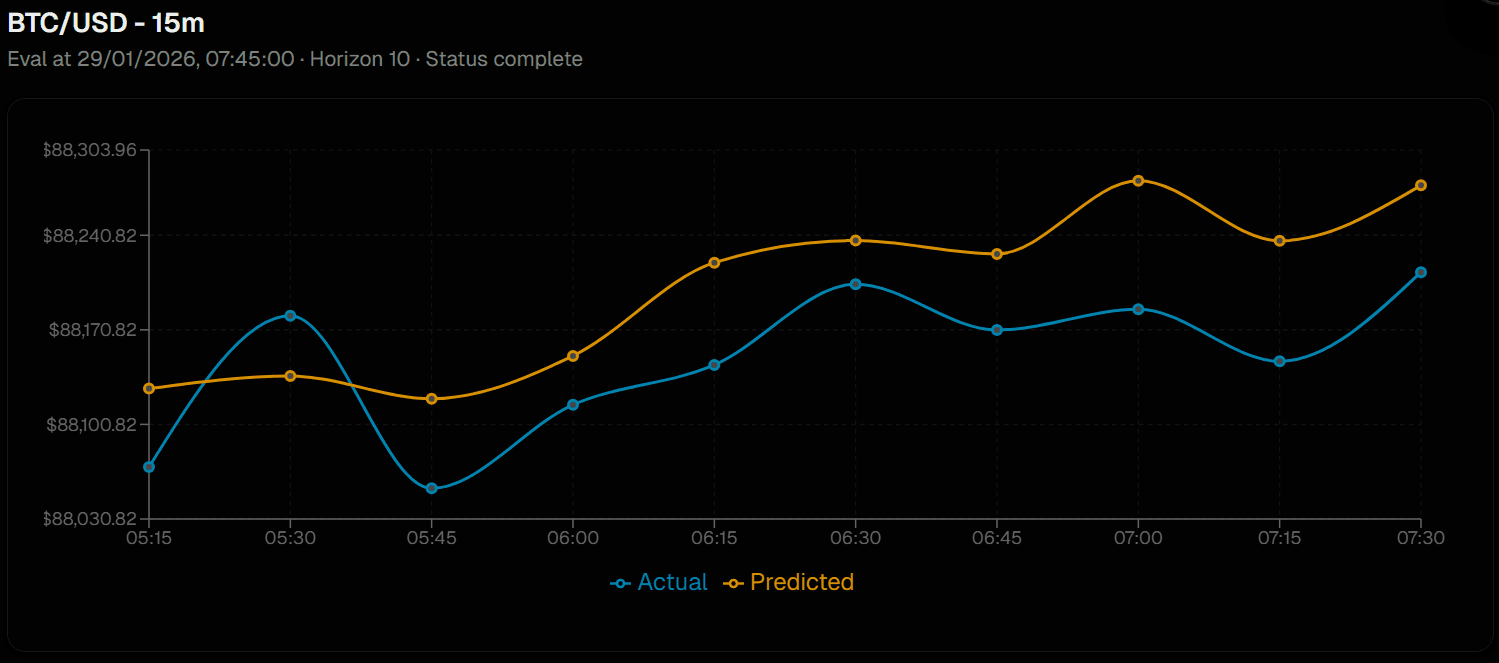

Actual vs Predicted Prices

Data Inputs

Crypto

CryptoHistoricalDataClient

Equities

StockHistoricalDataClient (coming soon)

Feature Matrix

[open, high, low, close, volume] as float64

Timeframes

Minutes, Hours, Days with multiplier (15m, 1h, 1d)

Feature Engineering

Window Size

200-500

Sample Shape

(window_size, 5)

Target

Next-step log return of close

r = log(close_{t+1} / close_t)

Data Split

Train: 70%

Validation: 15%

Test: 15%

Sequential split (no shuffling) to preserve time order

Scaling & Normalization

Feature Scaling

StandardScaler fitted on flattened training windows only

Target Scaling

Separate scaler fitted on y_train only

Leakage Prevention

Val/test data never seen during scaler fitting

Neural Network Architecture

Checking access...

Prediction & Evaluation

Checking access...

Note: All models have been tested on out-of-sample data to ensure realistic performance metrics. Past performance does not guarantee future results. These models are implementations based on academic research and have been adapted for our trading platform. Terms of Use